Ancient Cash Flow Secret | The King’s Cash | Session 8

Series: The King’s Cash | Session 8

Text: Proverbs 24:27

Work for your money then get your money working for you

This message highlights the wisdom of knowing the true state of your financial life. Careful attention to assets, expenses, and long-term needs helps prevent crisis and supports a stable, sustainable lifestyle rooted in stewarding what God has provided.

Here’s a thought: Albert Einstein called compound interest “the greatest mathematical discovery of all time.”

If I have it, I don’t share it. If I share it, I don’t have it. What is it? A secret. I have a secret to share with you – an ancient cash flow secret.

Show the animated version of Aesop’s Fable, “Goose that Laid the Golden Egg”

We can glean several moral lessons from this fable of Aesop, a legendary Greek storyteller who allegedly lived 600 years Before Christ. One lesson is similar to what we read in Proverbs 24:27, “Finish your outdoor work and get your fields ready; after that, build your house.” NIV

Keeping in mind that Proverbs 24:27 originated in an agricultural society, The Living Bible helps us to understand it in today’s setting, “Develop your business first before building your house.”

People who make financial progress:

Invest in Assets

Israelites, most of whom farmed land, needed to plough and sow seed (to get their fields ready) before they attended to more immediate creature comforts. Whether house should be taken literally (constructing a house) or figuratively (getting married and having a family), the principle is the same: it is important to have one's priorities straight. (from Bible Knowledge Commentary/Old Testament Copyright © 1983, 2000 Cook Communications Ministries; Bible Knowledge Commentary/New Testament Copyright © 1983, 2000 Cook Communications Ministries. All rights reserved.) In his commentary on Proverbs 24:27 Matthew Henry summarizes, “We must prefer necessaries before conveniences”.

Robert Kiyosaki, author of “Rich Dad Poor Dad”, teaches that your home is not an asset in which you invest but is a liability that brings expenses. Everyone needs a place to live and yes, real estate values will almost certainly increase over the long-term. The problem is that when you sell your home you will probably buy another that has also increased in value over time.

An asset is something that can generate cash flow and merely owning something doesn't necessarily mean that it's making you any money. For financial expert and author of The Wealth Chef, Ann Wilson, this is a vital consideration that many people overlook when they sum up their perceived wealth - particularly when it comes to the house that they live in.

“It's absolutely key for me that when people develop their wealth plan they understand that something that can bring income into your life is an asset, while something that causes money to flow out of your life is a liability,” says Wilson.

And in this sense, your primary residence is actually a liability. Even if it is paid off, it does not generate any income for you and it costs you every month in rates and maintenance. For Wilson, this is one of the most critical things that most people need to come to terms with in their personal financial plans.

This ancient cash flow secret was revealed in Proverbs 24:27 almost 3,000 years ago but most people have not taken the time to discover it or made the effort to apply it. This principle did not originate with a man; the Creator wove it into the fabric of creation.

Listen to these words of Jesus 2,000 years ago in Luke 19:11-27:

11 While they were listening to this, he went on to tell them a parable, because he was near Jerusalem and the people thought that the kingdom of God was going to appear at once. 12 He said: "A man of noble birth went to a distant country to have himself appointed king and then to return. 13 So he called ten of his servants and gave them ten minas.' Put this money to work,' he said, 'until I come back.' 14 "But his subjects hated him and sent a delegation after him to say, 'We don't want this man to be our king.' 15 "He was made king, however, and returned home. Then he sent for the servants to whom he had given the money, in order to find out what they had gained with it. 16 "The first one came and said, 'Sir, your mina has earned ten more.' 17 "'Well done, my good servant!' his master replied. 'Because you have been trustworthy in a very small matter, take charge of ten cities.' 18 "The second came and said, 'Sir, your mina has earned five more.' 19 "His master answered, 'You take charge of five cities.' 20 "Then another servant came and said, 'Sir, here is your mina; I have kept it laid away in a piece of cloth. 21 I was afraid of you, because you are a hard man. You take out what you did not put in and reap what you did not sow.' 22 "His master replied, 'I will judge you by your own words, you wicked servant! You knew, did you, that I am a hard man, taking out what I did not put in, and reaping what I did not sow? 23 Why then didn't you put my money on deposit, so that when I came back, I could have collected it with interest?' 24 "Then he said to those standing by, 'Take his mina away from him and give it to the one who has ten minas.' 25 "'Sir,' they said, 'he already has ten!' 26 "He replied, 'I tell you that to everyone who has, more will be given, but as for the one who has nothing, even what he has will be taken away. 27 But those enemies of mine who did not want me to be king over them — bring them here and kill them in front of me.'" NIV

The master in this parable did not want his servants simply to hide his money; instead, he wanted his servants to get his money working for him by investing and growing it. Likewise, our Lord entrusts us with finances so we will invest it, grow it, enjoy it and, of course, give it.

Beware of putting all your eggs in one basket. For every one person who has “struck it rich” by starting or investing in one business venture there could be a thousand who have lost it by risking it all.

King Solomon advises in Ecclesiastes 11:1-2:

1 Cast your bread upon the waters, for after many days you will find it again. 2 Give portions to seven, yes to eight, for you do not know what disaster may come upon the land. NIV

The New Century Version translates Ecclesiastes 11:1-2 this way:

1 Invest what you have, because after a while you will get a return. 2 Invest what you have in several different businesses, because you don't know what disasters might happen.

The principle is clear - diversify your investments in different kinds of businesses, real estate, precious metals, etc.

Ivan & Angelina Cooke explain how rich people buy liabilities that depreciate in value:

They use their money to purchase assets and then use their portfolio or passive income from the assets to purchase the same liabilities that the poor and middle class do. The difference in their spending is that their money doesn’t go out the window and down the toilet, never to be seen again. The money that the rich worked for goes to creating more money. In this way, their money begins working for them and they can retire rich. The best part is that even after they retire, their money begins to compound and they get richer and richer!

When Warren Buffett was asked for the secrets to his wealth he replied, “It's three things. Number 1, it's being born in America. Number 2 it is good genes, so I live long enough. Number 3, it's compound interest. Compound interest — people have no idea the power that it really has."

I can’t tell you how many times I have heard people say they can’t afford to save and invest money. They declare themselves to be poor & it becomes a self-fulfilling prophecy, going on to wear this identity for the rest of their lives. Tony Robbins recounts a story of a UPS employee who never made more than $14,000 a year, but set aside 20% of every paycheque and put it into company stock. The man saw the value of his investments soar to more than $70 million by the time he was 90 years old. The reality is that you can’t afford not to save and invest your money!

I recommend “The Wealthy Barber” by David Chilton. It is an easy book to read about a barber who saved, invested and grew his money over time.

My father bought his first farm at the age of 21. Through hard work and frugal living he paid it off then went on to invest more in real estate. He, his children and his grandchildren have enjoyed the benefits for years.

Many of us have played the classic game of Monopoly. I discovered years ago that the game is typically won or lost in the first few rounds around the board. While in the short-term it seems more attractive to hold on to your money it is actually to your advantage to buy every property you land on. This puts you in the position to gain rental revenue, add houses and hotels and to trade property. In other words, the sooner you get your money working for you the better off you will be at the end of the game.

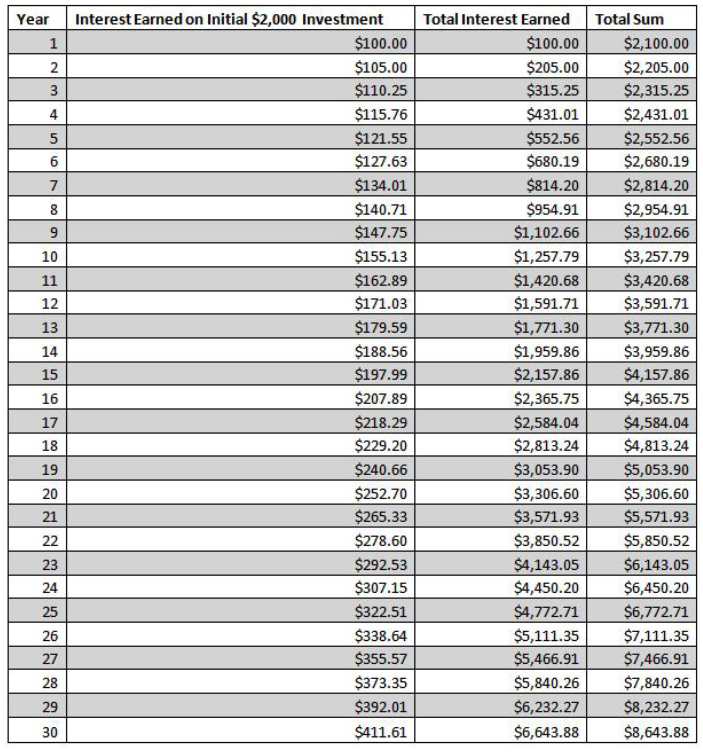

Use the power of time. Compound interest is most powerful over a long period of time. For example, if you invested $2,000 and gained a 5% return your investment would double in about 14 years. If all the money remained untouched, it would earn twice as much interest between years 15 through 28. In year 29, you’d effectively be earning 20% interest on the original investment, all without lifting a finger.

See for yourself:

The earlier you start, the better. Whether you’re in your mid-30s or mid-60s, it’s never too late to start saving. If you put away even $100 a month, starting now, compound interest will duly reward you — even in today’s low interest rate environment.

For example, at age 33, a $100-per-month ($1,200 annual) contribution at a 1.5% annual interest rate will turn into nearly $60,000 by age 70. If you start at age 66, this same investment amounts to just $5,000. Still, not bad. But, it clearly demonstrates that the longer you can let your investment work and earn interest for you, the better.

You can feed, starve or kill the goose that will lay golden eggs for you. In other words, compound interest can work for you or against you. Albert Einstein called compound interest “the greatest mathematical discovery of all time.”

Will you deny the lesser to gain the greater? Will you live for the short-term or the long-term?

People who make financial progress:

Invest in Assets

Spend on Liabilities

We came across this sign in a store window in Bergen, Norway: “Sale. Don’t think just buy.”

Here is a simple yet profound principle that could change your life: earn interest; don’t pay it. After you have income streams from your business and/or investments you have more cash to share, to travel and to buy consumer items.

Wealthy people know the difference between “bread” – when to eat what their labour, business and investments produce and “seed” – when to sow back into their business and investments - while most people do not. There can be other reasons but this is often why the rich keep getting rich and the poor keep getting poorer. The poor and middle class usually stay “poor” and “middle class” because of their financial attitudes and habits. Once they get more money than they need for expenses, they usually spend it on liabilities.

While the poor and middle class are spending their money on liabilities that depreciate in value and cost them money to maintain the rich are investing their money in assets that appreciate in value and are generating income. Go ahead and treat yourself occasionally, but think about the coffee you buy at Starbucks or Tim Hortons every day and how much money that translates into every year. This money would serve you much better in the long term if you were investing it rather than drinking it.

Identify an item that your children tend to waste money on – for example, candy, ice cream, or video games. Ask them how much the item costs. When they answer, say, "That's how much it costs today. But what does it cost in terms of what you're giving up?" When they look confused, help them calculate an average annual amount spent on their luxury – for example, $2.00 per day, four days a week adds up to $416.00 per year. Now compare this to the alternative of saving that money. Let's say your children buy a $2.00 treat just once a week instead. They save the rest – which comes to $312.00 per year.

Saving that money for forty years at a five percent interest rate will result in over $39,500.00! Be sure to point out that only $12,480.00 ($312 times forty years) was actually saved. The other $27,020.00 comes from compound interest.

You can make this life-changing decision today: will you be an investor or a consumer?

Are you unsure where to start? Check out www.soundmindinvesting.com.

After graduating from Lake Forest College in 1931, Grace was hired as a secretary at Abbott Laboratories, where she worked for more than four decades.

Grace never earned an amazing salary as a secretary. According to the Los Angeles Times, she got her clothes from garage sales. She lived in a one-bedroom house that was willed to her when a friend passed.

But in 1935, a few years after she started her job at Abbott Labs, she bought three shares of the company’s stock for about $60 per share. Her total investment was under $200.

Grace never sold those shares. Through dividends, share splits, and dividend reinvestment, when she died in 2010, her three-share purchase was worth $7 million. She left it all to her alma mater [Lake Forest College].

The two most important lessons from this story?

She started with $200.

She took advantage of the power of compounding — for 75 years!

People who make financial progress:

Invest in Assets

Spend on Liabilities

Work for your money then get your money working for you.